May 2025 Market Recap

Last Month in the Markets: May 2025

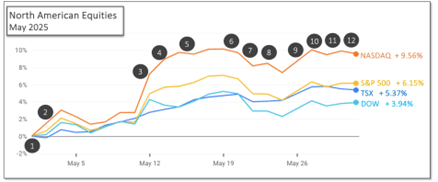

What happened in May?

The month began positively, and somewhat quietly. Entering the month, Canada was performing relatively well as the new government was preparing for the upcoming legislative session.

In the days leading up to mid-May, news broke that the U.S. and China had swiftly reached a more amicable trade arrangement, while continuing negotiations toward a comprehensive tariff and trade agreement. This optimism sent markets soaring. The gains on May 12th helped set a positive tone for the following week—momentum that largely held until the U.S. House of Representatives passed a substantial spending bill expected to significantly increase federal deficits.

At the end of the month, judicial rulings stayed and then reinstated Trump’s tariff program, European Union tariff delays, and a renewal of 50% steel tariffs kept rhetoric high, and equities largely held their gains until the end of the month.

More uncertainty, and volatility are predicted as trade negotiations and political whims continue.

Economic reports that influenced markets in May included:

1. April 30th – Canadian economic output declined

Canadian real Gross Domestic Product (GDP) was 0.2% lower in February, following a 0.4% increase in January. Goods producing industries fell 0.6%, services-producing industries slipped 0.1% in February. Mining, oil and gas extraction, construction, real estate, rental and leasing declined while durable goods, finance and insurance rose.

2. May 2nd – U.S. economy contracted in Q1, and job growth remained strong in April

American GDP decreased at an annual rate of 0.3 percent in the first quarter of 2025 according to the advance estimate released by the Bureau of Economic Analysis. For reference, in the fourth quarter of 2024, real GDP increased 2.4 percent.

U.S. nonfarm payroll employment increased by 177,000 in April and the unemployment rate was unchanged at 4.2 percent according to the Bureau of Labor Statistics’.

3. May 12th – Temporary truce between U.S. and China sent stocks soaring

U.S. tariffs on most Chinese goods have been reduced to 30% and China has reduced its tariffs on most U.S. goods to 10%. The size of the cuts to the proposed tariffs, on both sides, and the speed of the agreement contributed to the size of the surprise and the size of the increase for equity indexes.

4. May 13th and 14th – Positive inflation news contributed to equities rally

According to the Bureau of Labor Statistics, the all-items Consumer Price Index (CPI) increased 2.3% before seasonal adjustment over the last 12 months.

U.S. Producer Price Index fell 0.5% in April after being unchanged in March and increasing 0.2% in February. On an unadjusted basis, the index for final demand rose 2.4% for the 12 months ended in April.

5. May 16th – Moody’s downgraded U.S. government credit rating

The U.S. government had its creditworthiness rating downgraded by Moody’s, which followed the same conclusion reached previously by S&P Global ratings in 2011 and Fitch Ratings in 2023. Moody’s had held a perfect rating for the U.S. since 1917. The rating of the government’s ability to repay its debts is no longer at the highest level for all of the major ratings agencies.

6. May 20th – Canadian inflation slowed below Bank of Canada target

The Canadian Consumer Price Index (CPI) rose 1.7% year-over-year in April, down from a 2.3% increase in March. The lower inflation rate was led by energy prices that fell by 12.7% in April, after a 0.3% decline in March. However, inflation for food purchased in stores increased to 3.8% in April, following a 3.2% increase in March. The Bank of Canada attempts to limit the long-run average inflation rate to 2%.

7. May 21st – Legislative progress drove markets downward

The U.S. House of Representatives passed a “big, beautiful bill” that the non-partisan Congressional Budget Office predicts will increase the federal deficit by $3.8 Trillion over the next decade. On Wednesday, after the House narrowly passed bill that brings multitrillion dollar tax and spending cuts, U.S. equity markets fell.

The increasing deficit coupled with higher interest rates linked to the lower credit rating will bring higher borrowing costs and, ultimately, contribute further to the federal deficit.

8. May 23rd – Canadian retail sales continue to increase

Retail sales increased for the fourth consecutive quarter as six of nine subsectors saw increases. The largest increases were seen at motor vehicle and parts dealers, while sales at gasoline stations and fuel vendors fell in response to lower prices.

9. May 26th – Tariff delay for EU moved markets higher

Equities rallied after President Trump announced—just two days after its introduction—that a proposed 50% tariff on European Union imports would be delayed until July 9.

However, markets may continue to face volatility as the U.S. moves forward with a new 50% tariff on steel, prompting expected retaliatory measures from trade partners..

10. May 27th – King Charles delivered throne speech to Parliament

King Charles delivered the speech from the throne to open Parliament for the newly elected Liberal government under Prime Minister Mark Carney. The priorities to eliminate interprovincial trade barriers, develop diverse international trading partners, deliver a middle class tax cut, increase housing, reduce tax on new homes, and manage immigration were reiterated.

11. May 28th and 29th – Uncertainty over U.S. tariffs continued

The U.S. Court of International Trade (USCIT) ruled that Trump did not have the authority to impose the program of tariffs, which sent stocks upward. After a prompt appeal by the administration, a federal appeals court placed a temporary hold on the USCIT ruling. Stocks declined in response to the continuation of restrictive trade tactics.

12. May 29th and 30th – Canadian employment fell while GDP maintained its pace

Canadian payroll employment decreased by 54,000 in March following a decline of 40,200 in February. On a year-over-year basis, payroll employment was up 32,800 despite the last two months of decline.

Canadian GDP increased 0.5% in the first quarter of 2025, the same pace as the fourth quarter of 2024. Increased exports of passenger vehicles (+16.7%), industrial machinery, equipment and parts (+12.0%) were driven by the looming threat of U.S. tariffs.

On balance the economic and political news of May provided positive movement for equities. The lowering of tariff rates and delaying of tariff introductions pushed stocks higher. The judicial response, to this point, has been unhelpful for equity indexes.

What’s ahead for June and beyond?

The negotiations between the U.S. and multiple counties will dominate economic news for the foreseeable future. Prime Minister Mark Carney described the situation and Canada’s planned response in a speech in early April. While the actions of the U.S. president may not be predictable, the direction that the Canadian government will take is clear.

In more practical and mundane matters, the Bank of Canada and Federal Reserve will deliver their next interest rate announcements on June 4th and June 18th, respectively. Central banks are attempting to protect domestic economies while facing significant uncertainty regarding trade restrictions and tariffs originated by the U.S. President.