February 2026 Market Recap

Last Month in the Markets: February 2 – 27, 2026

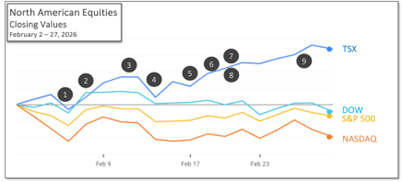

What happened in February?

The economic events of February were overshadowed by the political and military actions that occurred on the last day of the month following the close of markets on February 27.

Nonetheless, events that influenced markets in February included:

1. February 5 – European Central Bank held rates unchanged

The European Central Bank held its three key interest rates unchanged. The outlook is still uncertain, owing partially to ongoing global trade policy uncertainty and geopolitical tensions,” according to its monetary policy decision.

2. February 6 – Canadian employment and American unemployment disappointed

Employment edged down in January (-25,000; -0.1%), and the employment rate decreased 0.1 percentage points to 60.8%,” according to the most recent Labour Force Survey.

In 255 of 387 U.S. metropolitan areas, the unemployment rate in December 2025 was higher than one year earlier, according to the Bureau of Labor Statistics. National unemployment was 4.1%, up from 3.8% in December 2024.

3. February 11 – U.S. monthly jobs growth highest of Trump’s second term

The U.S. Bureau of Labor Statistics (BLS) released its delayed Employment Situation Summary. Total nonfarm payroll employment rose by 130,000 in January, and the unemployment rate changed little at 4.3%. For context, in 2023, 2024, and 2025, monthly job gains averaged 210,000, 122,000, and 15,000 respectively.

4. February 13 – U.S. CPI and corporate performance improved

The U.S. Consumer Price Index rose 0.2% in January and 2.4% on a year-over-year basis, according to the release from the BLS. The latest figures represent an improvement, but the year-over-year rate remains above the Federal Reserve’s goal of a 2% average.

5. February 17 – Canadian consumer prices dipped

Canada’s Consumer Price Index (CPI) rose 2.3% on a year-over-year basis in January, down slightly from its 2.4% increase in December. The price of gasoline, which has fallen almost 17% since January 2025, was the largest contributor to the deceleration in headline inflation.

Core inflation, which excludes food and energy, rose 2.4% last month and continues to edge downward toward the Bank of Canada’s 2% goal.

6. February 19 – Tariffs had no impact on U.S. trade balance, increased Canada’s deficit

The U.S. trade deficit was $901.5 billion in 2025, down just 0.2% (-$2.1 billion).

The future of Trump’s tariffs was complicated by a U.S. Supreme Court decision that the use of the International Emergency Economic Powers Act (IEEPA) to impose tariffs was unlawful in a 6–3 ruling. Trump immediately responded with 10% tariffs, later increasing them to 15% using different legislation.

In the wake of Trump’s tariffs, Canada’s trade deficit grew to $31.3 billion in 2025, the highest level since the pandemic. Exports to the U.S. dropped 5.8%, and imports from the U.S. fell 2.9%. The trade surplus with the U.S. narrowed to $81.6 billion in 2025, down from $101.3 billion in 2024.

7. February 20 – U.S. GDP growth slowed in Q4

U.S. Gross Domestic Product rose just 1.4% in the fourth quarter of 2025. Economic growth was well below expectations, with government spending dropping temporarily due to the U.S. government shutdown.

8. February 20 – U.S. inflation rose again

The Federal Reserve’s preferred inflation indicator, the Personal Consumption Expenditures Price Index, increased as it rose 0.1% to 2.9% in December.

9. February 27 – Canadian GDP fell in Q4

Canadian real gross domestic product (GDP) declined 0.2% in the fourth quarter of 2025 after rising 0.6% in the third quarter. Much of last year’s decline can be attributed to decreased exports to the U.S.

What’s ahead for March and beyond?

February ended with joint U.S. and Israeli attacks against Iran’s leadership, nuclear program, and infrastructure. Iran responded by attacking American and Israeli interests across the region regardless of their location.

Markets responded quickly on the first trading days of March. Monday saw gold and oil rise sharply. North American equity markets were flat on March 2, then tumbled at the open the following day.

In the medium and long term, inflation, employment, economic growth, and monetary policy will continue to influence markets. In the near term, the conflict across the Middle East and its direct effects on energy supply and prices will have a significant impact.

The VIX Volatility Index, which measures market expectations of near-term price changes in the S&P 500, has also risen sharply. Volatility will remain elevated as long as the conflict continues and defensive and offensive actions remain uncertain.