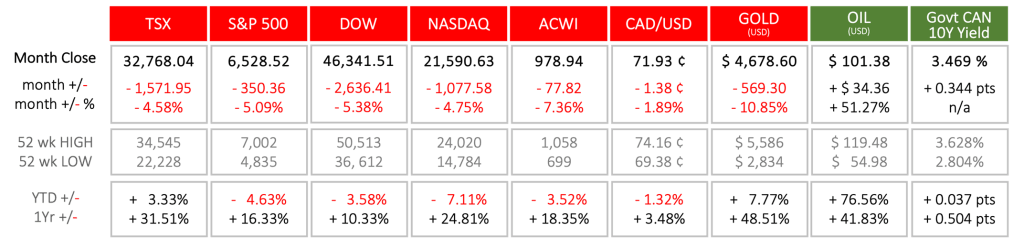

March 2026 Market Recap

Last Month in the Markets: March 2 – 31, 2026

What happened in March?

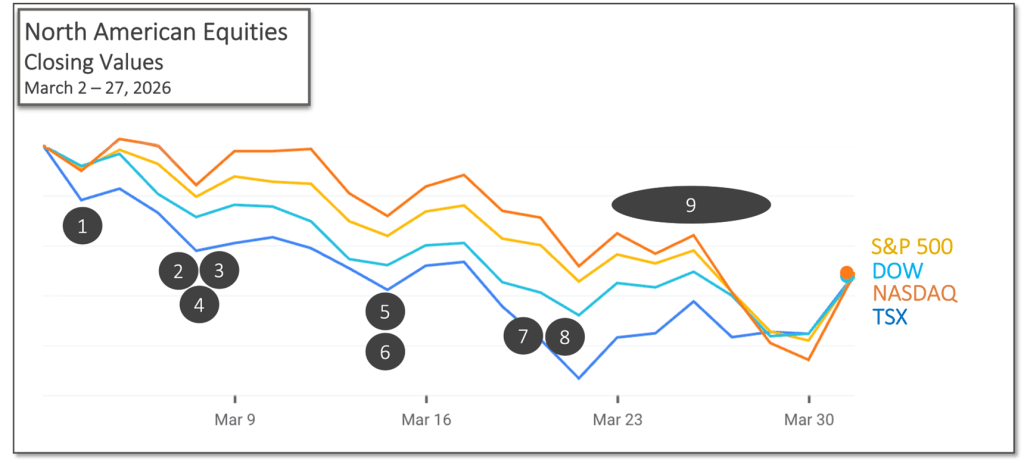

Nearly every market move was controlled, or at least heavily influenced, by the U.S. attack on Iran that began at the end of February. Two days of conflict preceded the opening of trading on March 2, and the war continued unabated through the end of the month and beyond. The first three weeks of March were marked by a nearly continuous series of losses for North American equity indexes, which declined between 4.5% and 9%.

On March 23, Donald Trump stated that discussions with Iran’s leadership to end the war were progressing well. Markets reacted immediately: oil prices dropped more than 10%, gold fell by 5%, and equities rose by 2% after the opening bell on March 24, highlighting the relationship between uncertainty-driven commodity prices and equity values. Progress in negotiations that would allow oil shipments through the Strait of Hormuz will greatly influence oil prices and equity markets in the near term.

Until a full resolution to the conflict is achieved, political and military uncertainty is expected to keep the VIX Volatility Index elevated.

Events that influenced markets in March included:

1. March 3 – Quarterly U.S. corporate results remained strong

Despite geopolitical challenges, a bright spot for equities was the conclusion of fourth-quarter earnings for the S&P 500. Approximately 73% of companies exceeded earnings-per-share estimates, and earnings growth reached 14%, marking the fifth consecutive quarter of double-digit growth.

2. March 6 – Oil prices rose and equity values fell

Oil prices rose more than 35% in the first week of March, closing at nearly $91 USD per barrel for the West Texas Intermediate (WTI) benchmark. Rising energy costs pressured corporate valuations (excluding many energy-related stocks), as higher input costs threaten future revenues and profits. Increased energy prices are also expected to push up inflation, which may delay or reverse anticipated rate cuts by the Federal Reserve, the Bank of Canada, and other central banks, potentially slowing economic growth.

3. March 6 – U.S. experienced a significant employment decline

The loss of U.S. jobs added to market concerns. The Bureau of Labor Statistics reported that payrolls declined by 92,000 in February, while the unemployment rate remained relatively unchanged at 4.4%. The last time the Bureau released a notably disappointing jobs report, President Trump dismissed the lead statistician.

4. March 6 – Canadian trade diplomacy supported the economy

Prime Minister Mark Carney pursued trade agreements with more reliable global partners, excluding the United States. Agreements were reached with India, Australia, and Japan, and further bilateral economic integration is under negotiation.

5. March 13 – U.S. economic growth slowed in Q4 2025

U.S. Gross Domestic Product (GDP) grew by just 0.7% in the fourth quarter of 2025, according to the Commerce Department’s latest revision. A government shutdown contributed significantly to the slowdown. For the full year, GDP growth was 2.1%.

6. March 13 – Canadian employment declined sharply

Canada’s Labour Force Survey showed employment decreased by 84,000 in February, while the unemployment rate rose by 0.2% to 6.7%. Employment declined across both goods-producing and services-producing industries by 28,000 and 56,000, respectively.

7. March 13 – U.S. inflation remained below 3% (for now)

The Bureau of Economic Analysis reported that the Federal Reserve’s preferred inflation measure, the Personal Consumption Expenditures (PCE) Price Index, rose 2.8% year-over-year in January. Core PCE, which excludes food and energy, increased by 3.1%, consistent with December levels. However, rising energy prices since the onset of the conflict were not yet reflected in these figures.

8. March 18 – North American interest rates remained unchanged

The Bank of Canada held its overnight rate steady at 2.25%, where it has remained since the 0.25% reduction on October 29. Although Canadian inflation slowed in February, Governor Tiff Macklem noted that rising global energy prices would likely push inflation higher in the coming months.

The U.S. Federal Reserve maintained its federal funds rate in the range of 3.5% to 3.75%, following a total reduction of 0.75% between September and December 2025. Fed Chair Jerome Powell indicated that near-term inflation expectations have risen, largely due to higher oil prices stemming from supply disruptions in the Middle East. Updated projections also show increased inflation expectations since December.

9. March 19 – European Central Bank followed suit

The European Central Bank (ECB) also held interest rates steady. While inflation in Europe has hovered near 2% over the past year, officials indicated that higher energy prices linked to the conflict would likely push inflation above target in the short term.

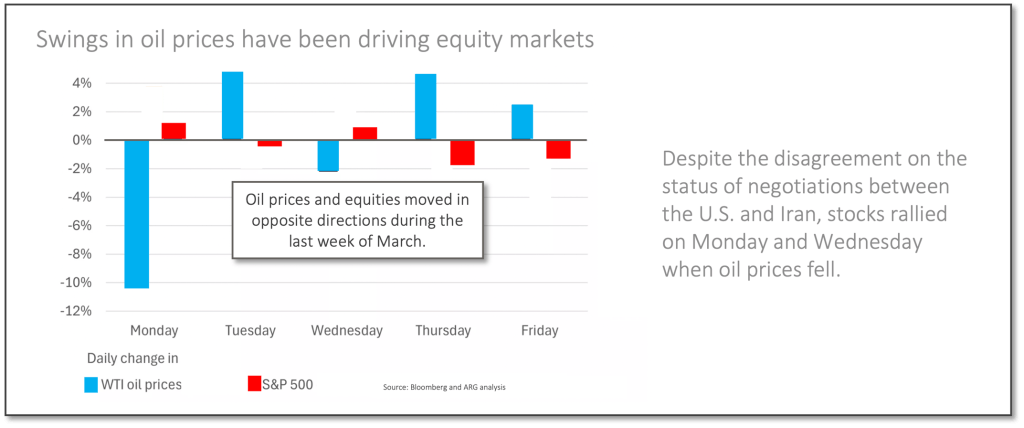

10. March 23–27 – Oil prices and equities moved inversely

During the final full week of March, oil prices and equities moved in opposite directions. As oil prices rose, equities declined, and vice versa. On Monday, President Trump announced progress toward negotiations to end the conflict, leading to a sharp drop in oil prices and a corresponding rise in equity markets.

What’s ahead for April and beyond?

The relationship between geopolitical tension—particularly as reflected in oil prices—and capital markets is expected to persist in the near term. The supply shock caused by disruptions in the Strait of Hormuz bears similarities to the oil embargo imposed by the Organization of Arab Petroleum Exporting Countries (OAPEC) in the 1970s.

If higher oil prices lead to increased inflation, monetary policy may be affected. Previously, improving inflation trends and weakening employment data had raised expectations for interest rate cuts by the Bank of Canada and the Federal Reserve. However, CME’s FedWatch tool now suggests that U.S. rate cuts are unlikely in the near term, while Canadian rates are already lower than those in the U.S. Upcoming rate decisions will depend on updated inflation data, which will incorporate the impact of rising energy prices.

The political risks associated with higher inflation and slower economic growth may pressure U.S. leadership to resolve the conflict, particularly as midterm elections approach. A resolution to the war in Iran would likely reduce market volatility and geopolitical risk.

On April 1, Donald Trump delivered a 20-minute primetime address on the Iran conflict. His remarks were quickly reflected in commodity markets, with oil prices rising an additional 10%, further illustrating the strong link between geopolitics, military action, the Strait of Hormuz, and commodity pricing.